Authors: DJ Rich, Patrick Hop

How do factor premia vary over time examines excess (of cash) returns of widely known investment strategies, expressed as factors that account for a large proportion of cross-sectional asset price variations. The factors explored are value, momentum, defensive and carry, with data going back to the 1920s.

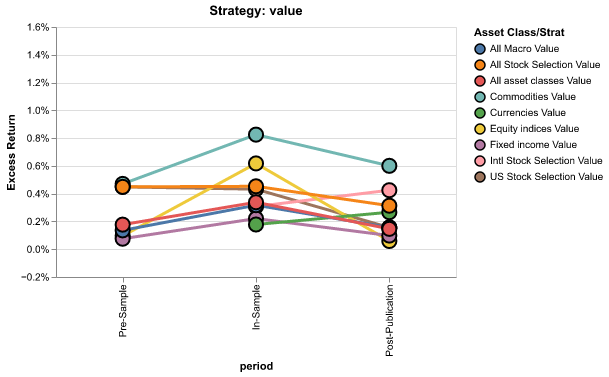

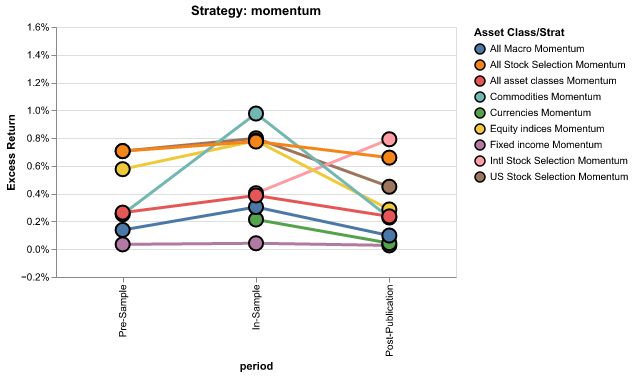

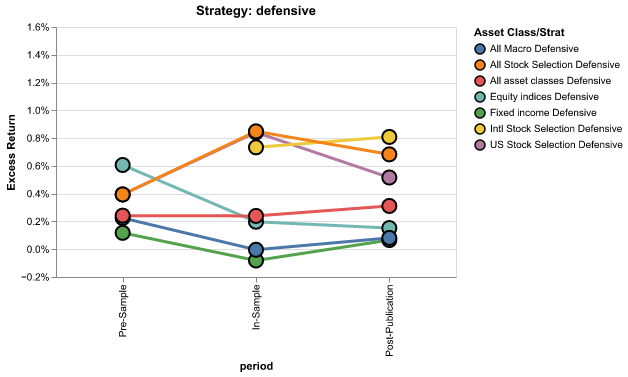

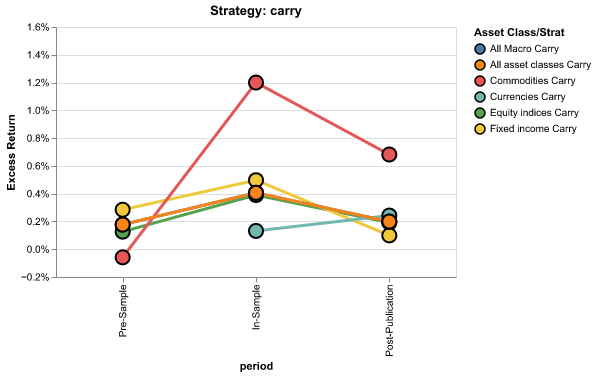

Consider the following data from the aforementioned paper. The authors constructed portfolios as per each of the classically known factors. For each strategy, the authors delineated three periods:

(1) Pre-sample: All months prior to the first month considered in the construction of the strategy in its first major publication.

(2) In-sample: The months used to construct the strategy.

(3) Post-publication: All months following the strategy’s publication date.

A strategy’s in-sample period is expected to show the highest returns, since there is presumably some data-mining bias and no market knowledge of the strategy. For the post-publication period, the strategy is expected to have the lowest returns, since market knowledge of the strategy should compete away returns and it serves as a true out-of-sample test free of data mining bias. For the pre-sample period, no market knowledge and no data mining bias are counteracting forces, so we expect a mid-level return. And indeed, this is typically observed. Below, we show average excess returns for each strategy (factor) category. Each period spans multiple decades, so large differences correspond to statistically significant ones.

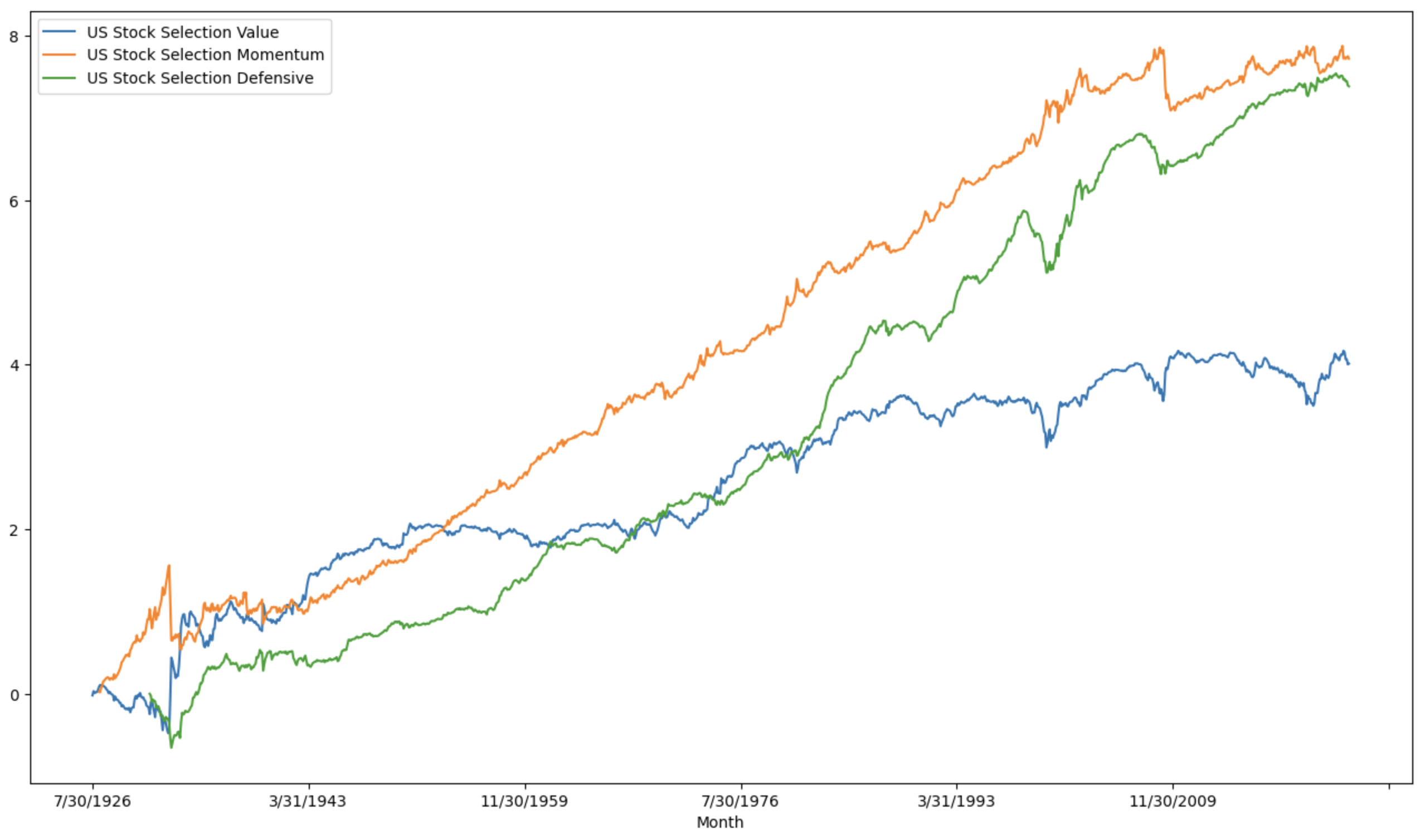

A subset of these strategies can be backtested all the way through the American great-depression. Below we consider the cumulative excess performance of US stock-selection value, momentum, and, defense over an almost 100 year period:

An explanation for why such returns persist, despite these strategies being in the public domain for decades, helps an investor accept their usage in a long-term portfolio. Some possible explanations:

(1) Limits to arbitrage: insufficient arbitrage capital, market frictions, existence of noise traders, costly & risky arbitrage

(2) Behavioral biases: prospect theory, hindsight bias, lottery ticket style preferences, liquidity preferences, disposition effect

(3) Supply-demand effects: insufficient liquidity, market microstructure dynamics, meta-orders

(4) Diverse agents: heterogenous expectations and asymmetric information among market participants

(5) Trading restrictions: a significant proportion of market participants are restricted from short-selling and using financial leverage

(6) Risk premia: some asset mispricings are entirely rational and represent risks that other market participants rightfully don’t want